Contributed by Charles Brown, Farm Management Specialist, Iowa State University Extension and Outreach, crbrown@iastate.edu, 641-673-5841

In 2018, again some Iowa farmers are suffering the extremes of drought in the Southeast and floods in the North and Northeast. Both losses due to drought and flooding are an insurable loss under multi-peril crop insurance. Another dynamic added to the mix this year is yield loss due to chemical drift or misapplication, which is not a covered loss under multi-peril crop insurance. Especially in Southeast Iowa, due to drought conditions, again there will be claims for losses on corn and soybeans.

In 2018, again some Iowa farmers are suffering the extremes of drought in the Southeast and floods in the North and Northeast. Both losses due to drought and flooding are an insurable loss under multi-peril crop insurance. Another dynamic added to the mix this year is yield loss due to chemical drift or misapplication, which is not a covered loss under multi-peril crop insurance. Especially in Southeast Iowa, due to drought conditions, again there will be claims for losses on corn and soybeans.

Important Point: Do not destroy a crop, comingle grain from previous years or different owners or harvest for silage before contacting your insurance agent. Bins must be measured before comingling grain. When in doubt call your agent.

Question: How many of Iowa’s corn and soybean acres are covered by crop insurance?

Iowa farmers planted 23.2 million acres of corn and soybeans in 2018. Approximately 90% of those acres have been insured using Revenue Protection (RP) multi-peril crop insurance. These insurance policies can guarantee various levels of a percentage of the farm’s average yield times the higher of the projected price (average futures price in the month of February) or the harvest price (average futures price during the month of October), using the November 2018 futures contract for soybeans and the December 2018 futures contract for corn. Most farm operators carry a guarantee of their APH from 65% to 85% level of coverage. The projected prices (futures average prices in February 2018) were $3.96/bu for corn and $10.16/bu for soybeans, respectively.

Question: What should an insured farmer do once a crop loss is recognized?

- Notify the insurance agent within 72 hours of the discovery of damage, but not later than 15 days after the end of the insurance period. A notice of loss can be made by phone, in writing or in person. Although drought loss is not immediate, farmers should contact their agent as soon as they feel a loss is present.

- Continue to care for the crop using “good farming practices” and protect it from further damage, if possible.

- Get permission from the insurance company, also referred to as your Approved Insurance Provider (AIP), before destroying or putting any crop to an alternative use.

Question: Who will appraise the crops and assess the loss?

The crop insurance company will assign a crop insurance adjuster to appraise the crop and assess the loss. The insured farmer must maintain the crop until the appraisal is complete. If the company cannot make an accurate appraisal, or the farmer disagrees with the appraisal, the company can have the farmer leave representative sample areas.

These representative sample areas of the crop are to be maintained – including normal spraying if economically justified – until the company conducts a final inspection. Failure to maintain the representative sample areas could result in a determination that the cause of loss is not covered. Therefore no claims payment to the producer.

Once appraised the crop can be released by the company to be:

- Destroyed – through tillage, shredding or chemical means; or

- Used as silage or feed.

Question: Once released, may I harvest my corn as silage for feed?

Check with your crop insurance company. In a county where corn can be insured as grain only, the corn will be released, or harvested as silage and/or sold as feed. Any grain will be counted as production for your claim. In a county where corn can be insured as silage, the harvested silage will be counted as production.

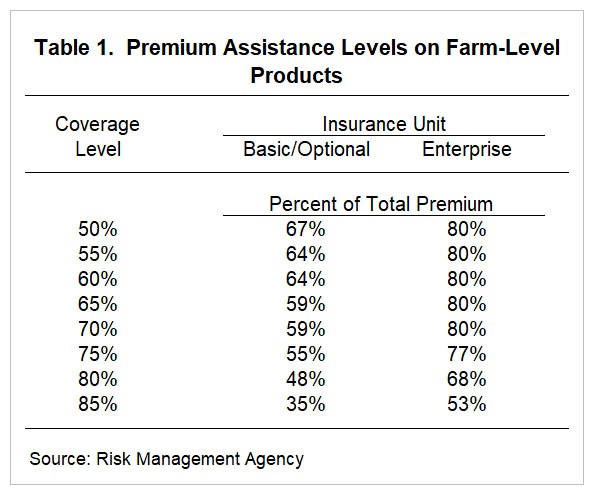

Question: What is the difference among insurance units?

Many farmers have chosen to insure their crops using enterprise units in order to pay less expensive insurance premiums. Under enterprise units, losses are calculated by crop by county. Therefore all the corn planted by a farmer is a given county would be added together to determine a loss. If a farmer has chosen optional units, then losses are calculated by crop by field unit. Premiums are typically higher if choosing optional units, but a good yield on one field does not cancel out the loss on another field.

Question: When will farmers be receiving indemnity payments for their crop insurance losses?

Adjusters will be busy with the increase in losses in Southeast Iowa. As soon as you are finished harvesting notify your insurance agent and an adjuster will be assigned to you. Insurance companies cannot defer payments to the next tax year, but claims adjusted late in the year may not be paid out until the following year.

Question: What is the maximum price that the harvest time indemnity price (average October futures price) can reach?

The maximum harvest indemnity price values for 2018 are twice of the projected price; or $7.92/bu for corn and $20.32/bu for soybeans, respectively.

Question: Can indemnity payments for drought be deferred for income tax purposes until 2019?

A taxpayer using the cash method of accounting claims the income in the year they receive the payment. The insurance company will send the insured a 1099 showing the amount and tax year to report the income.

A farmer, if they are using the cash method of accounting for reporting taxes, can elect to defer crop insurance payments if the loss is due to yield loss and they normally sell more than 50% of their crop the year following harvest. They cannot defer any loss that is due to price loss. Farmers that are using the accrual method of accounting for reporting taxes cannot defer crop insurance payments.

Question: Will I be asked to provide proof of my bushels this year for crop insurance verification?

All multiple peril crop insurance users are subject to production verification on a random basis. If a claim that exceeds $200,000 is filed for an individual crop and policy, verification of production is automatically required by regulation. This also requires a 3 year audit.

An agricultural economics and business website.